MELBOURNE · FITZROY · TUESDAY · 9:14 AM

The café smells like cardamom and fresh bread. It’s a Tuesday — quiet enough that Sarah, who owns this place, finally has five minutes to sit down with her phone.

She refreshes her email.

There it is. The subject line she’s been waiting three weeks for.

“We regret to inform you that your application has been unsuccessful.”

Third time. Same answer.

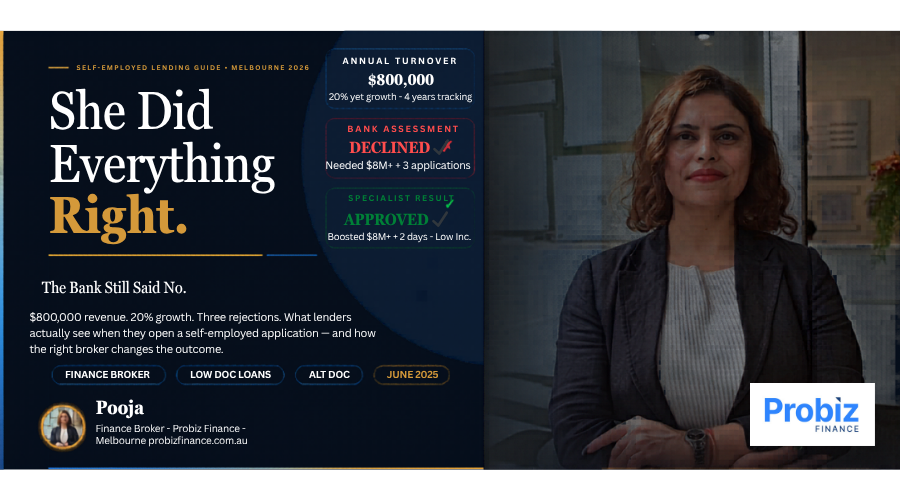

Sarah has run this café for four years. Revenue is up 20% year-on-year. She has no defaults, no credit issues, a loyal customer base, and a plan to open a second location that her accountant has reviewed and signed off on. She has $800,000 in annual turnover and needs $1,000,000 to grow.

The bank doesn’t care.

This guide is about the gap between those two things. About what lenders actually see when they open a self-employed application, what they’re trained to look for in the first 90 seconds, and — critically — how to close that gap before you submit a single form.

And it’s about what Sarah did next, which changed everything.

Here’s the uncomfortable truth about being self-employed in Australia in 2026: your tax return is lying about you.

Not maliciously. Not illegally. In fact, the more diligently you’ve managed your taxes — claiming every eligible deduction, structuring your income correctly, running legitimate expenses through the business — the more unflattering your tax return looks to a lender’s credit algorithm.

Think about that for a moment.

The Self-Employed Tax Paradox

|

This is the trap. Your accountant is doing their job perfectly. The bank is doing its job perfectly. And you’re stuck in the middle with a thriving business and a declined application.

Sarah’s problem wasn’t her café. It was that nobody had ever explained to her that lenders and the ATO are operating on fundamentally different definitions of income — and that before you apply for a loan, you need to bridge that gap deliberately.

So let’s talk about how.

Most people imagine a loan assessor sitting down, reading through their whole application thoughtfully, and making a considered judgement. The reality is different.

A credit assessor at a major bank might review 15 to 20 applications in a day. They’re not reading. They’re scanning. And they’re scanning for specific things — not to find reasons to approve you, but to quickly eliminate files that don’t fit the template.

Here’s what they look at first, in roughly this order:

Notice what’s not on that list: your actual revenue, your growth trajectory, your customer retention, your industry reputation, or your business plan. The traditional bank loan process was designed for salaried employees, and it’s been adapted for self-employed borrowers rather than built for them.

This is why Sarah was rejected three times despite a genuinely strong business. She was sending a full doc application to lenders whose scorecards weren’t designed to read it correctly.

The four major banks are not the only game in town — not even close. And for self-employed borrowers, they’re often not the right starting point at all. Here’s the actual landscape:

The traditional path. Requires two years of tax returns, financial statements, and BAS. Best rates, slowest approval, most restrictive criteria. Suitable if your financials cleanly and consistently show strong assessable income — which for many self-employed borrowers, they don’t.

This is where things get interesting. Low doc loans were specifically created for borrowers whose income is real but difficult to document through conventional means. Instead of two years of tax returns, you can typically provide:

The interest rate will be marginally higher than a full doc loan — typically 0.5% to 1.5% — but the difference in who can access this product is enormous. Sarah would have been approved on low doc. Her BAS statements told the real story of her café.

Alt doc loans go a step further. Lenders assess your income through alternative evidence — an accountant’s letter, rental income statements, or business bank statements — without requiring tax returns at all. If you’ve recently started your business, restructured, or gone through a period where your financials don’t tell the full story, alt doc may be the right path.

If your funding need is tied to purchasing equipment, vehicles, or machinery, equipment finance sits in its own category — and it’s often significantly easier to access than a general business loan. The asset secures the loan, which reduces lender risk substantially.

Before approaching any lender — before even talking to a broker — do this audit on your own situation. It takes 20 minutes and will tell you more about your borrowing position than three bank appointments.

Pull out your last two tax returns. Look at your net taxable income. Now ask your accountant which add-backs may apply: depreciation, one-off expenses, non-recurring write-offs. Many lenders will allow these to be added back to your income figure, sometimes increasing your assessable income by 20–40%.

Open the last 6 months of your business bank statements. Look for three things:

Simple but critical. If your ABN is under 12 months old, most full doc and low doc lenders won’t consider you. You’re looking at alt doc and specialist lenders only — which is fine, but you need to know that going in.

Both personal and business. Use a service like Equifax or Experian to pull your own report before a lender does. Any defaults, court judgements, or excessive recent enquiries need to be understood before you apply — not discovered during the assessment.

Here’s why this matters: every time a lender pulls your credit file, it registers as an enquiry. Multiple enquiries in a short period — which happens when borrowers apply to several lenders without a broker — actively damages your credit score. A broker submits one application, to the right lender, first time.

Following the RBA’s rate adjustments through 2025 and into 2026, the business lending environment has changed in ways that create both challenges and opportunities for self-employed borrowers.

The challenge: Lenders have tightened their serviceability buffers. Where some lenders previously tested your ability to repay at 2% above the loan rate, many are now testing at 3% or higher. For self-employed borrowers with already-compressed assessable income, this can meaningfully reduce borrowing capacity.

The opportunity: Non-bank lenders — fintechs, specialist credit providers, and wholesale lenders — are aggressively competing for the self-employed market that the majors are underserving. Some of these lenders have more flexible serviceability models, faster approval timelines (sometimes 24–48 hours), and a genuine understanding of variable income structures.

The catch: most borrowers never find these lenders because they don’t advertise to consumers. They work through brokers. This is one of the most practical, concrete reasons why working with a finance broker who specialises in self-employed lending changes your outcomes — not because brokers work magic, but because they have access to lenders you simply cannot reach on your own.

If you’re reading this before the end of the 2025–26 financial year, pay attention.

The catch is timing. Equipment finance approvals typically take 3–10 business days. The asset needs to be installed and in use before June 30, not just ordered. If you’re planning to use this strategy, the time to start the finance process is now — not in the last week of June.

Sarah didn’t apply to a fourth bank. She called a broker — specifically, a finance broker who works with self-employed borrowers in Melbourne.

In their first conversation, the broker asked her something none of the banks had asked: “What does your BAS history look like, and can your accountant provide an income declaration?”

That question told Sarah something important: this person was thinking about her situation differently. Not as a self-employed applicant who didn’t fit the template — but as a business owner whose income story needed to be told in the right language, to the right lender.

The broker identified a specialist non-bank lender who offered low doc lending to hospitality businesses with 2+ years of BAS history. Sarah’s BAS statements showed consistent quarterly revenue growth of 20% year-on-year. Her accountant prepared a one-page income declaration. The broker packaged it, negotiated the rate, and managed the whole process.

The second location opened four months after that.

I’ve reviewed hundreds of declined applications as a finance broker. The rejections cluster around the same five mistakes, almost without exception:

Walking into a major bank branch with a low doc income profile. The branch can only offer what the branch sells. This isn’t a moral judgement — it’s a product mismatch.

One of the first things an assessor looks for. Mixed accounts make income analysis complicated and raise questions. Clean, separated accounts take this issue off the table entirely.

If you’ve recently changed from a sole trader to a company, or restructured your trust, your business effectively has a new ABN history. Many lenders count trading history from the current structure, not from when the business started. Know where you stand before applying.

An ATO debt with no formal payment arrangement is a significant red flag. An ATO debt with an active, consistently-met payment plan is manageable. The difference isn’t the debt — it’s whether you’ve addressed it proactively.

Every direct application triggers a credit enquiry. Multiple enquiries in a short window signal financial stress to lenders and can lower your score. A broker runs one pre-assessment, identifies the right lender, and makes one application.

The most expensive thing a self-employed borrower can do is apply for a loan without understanding their position first. Not because applications cost money — they don’t — but because a declined application costs you time, costs a credit enquiry, and can close doors with other lenders for months.

The smartest move is a pre-assessment conversation with a broker who specialises in self-employed lending. Bring your last 6 months of bank statements, your most recent BAS, and a rough figure of what you need. That conversation — which costs you nothing — will tell you:

Please feel free to contact us. We’re super happy to talk to you.

Feel free to ask anything.

Help us improve. Our team will personally reach out to make things right.